CHAPTER 1:

Introduction to Microeconomics

Microeconomics

In every area of human enterprise and endeavor, there's a big picture and a little picture, the macro and the micro. The macro looks at things through a wide-angle lens; the micro looks at things through a narrow-focus lens. This is also true in economics and its two branches, macroeconomics and microeconomics.

Microeconomics

In every area of human enterprise and endeavor, there's a big picture and a little picture, the macro and the micro. The macro looks at things through a wide-angle lens; the micro looks at things through a narrow-focus lens. This is also true in economics and its two branches, macroeconomics and microeconomics.

Macroeconomics studies large-scale phenomena in the national economy, and even

in global economies, because they're interrelated. These would include central

bank interest rates, national employment numbers, gross national product figures, trade deficits or

surpluses, foreign currency exchange rates,

and other major economic activity and data.

By contrast, microeconomics studies a limited, smaller area of economics, including the actions of individual consumers and businesses, and the process by which both make their economic decisions – buying, selling, the prices businesses charge for their goods and services and how much of these goods and services they produce and or offer.

Microeconomic study reveals how start-up businesses have determined the competitively successful or unsuccessful pricing of their goods and services based on consumer needs and choices, market competition and other financial and economic formulas.

Microeconomics also studies supply-demand ratios and its effect on consumer spending and business decision-making.

At the heart of consumer purchasing is the concept of utility, a classic economic idea. Utility is the term applied to a consumer's satisfaction after the purchase of some product or service. Because a consumer's feeling of satisfaction may be impossible to precisely quantify in actual numbers, the concept may seem impractical. But a reasonably close approximation is useful to businesses, and may also be useful to the individual consumer who can probably measure that feeling of satisfaction with a "gut" reaction.

These concepts are explained in the following tutorial on microeconomics. The information is both practical and theoretical, and fascinating as well. It will provide the reader with a big picture of small picture economics…

By contrast, microeconomics studies a limited, smaller area of economics, including the actions of individual consumers and businesses, and the process by which both make their economic decisions – buying, selling, the prices businesses charge for their goods and services and how much of these goods and services they produce and or offer.

Microeconomic study reveals how start-up businesses have determined the competitively successful or unsuccessful pricing of their goods and services based on consumer needs and choices, market competition and other financial and economic formulas.

Microeconomics also studies supply-demand ratios and its effect on consumer spending and business decision-making.

At the heart of consumer purchasing is the concept of utility, a classic economic idea. Utility is the term applied to a consumer's satisfaction after the purchase of some product or service. Because a consumer's feeling of satisfaction may be impossible to precisely quantify in actual numbers, the concept may seem impractical. But a reasonably close approximation is useful to businesses, and may also be useful to the individual consumer who can probably measure that feeling of satisfaction with a "gut" reaction.

These concepts are explained in the following tutorial on microeconomics. The information is both practical and theoretical, and fascinating as well. It will provide the reader with a big picture of small picture economics…

LEARNING OUTCOMES

At the end of this chapter, you/students

should be able to understand:

The definition of microeconomics

Economic resources

Classification/Types of goods

The field of economics (Microeconomics and

Macroeconomics)

The concept of economic problems

(scarcity, choice and opportunity cost)

The production possibilities curve

Basic economic problems

Solving basic economic problems

The economic system

The merits and demerits of economic

systems

INTRODUCTION

This chapter gives a brief description of

economics in general.

Several economic concepts and terms, such

as scarcity, choice, and opportunity

cost, will be introduced.

Besides that, we will discuss the major

problems and issues that economics attempt to address.

Microeconomics is the study of:

How individuals and societies use limited

resources to satisfy unlimited wants, and

How such choices are made.

Economics is the study of how individuals

and economies deal with the fundamental problem of scarcity. Several known

economists have defined economics as follows.

Economics as a Science of Wealth

According to Adam Smith, economics is the

study of a nation's accumulation of wealth.

F A Walker defined economics as a branch

of knowledge associated with wealth.

J B Say also stated that economics is a

field of science that examines wealth.

These economists are of the opinion that

the study of economics will enable

individuals, communities, and countries to accumulate wealth and become

prosperous.

Economics as a Science of Material Welfare

Alfred Marshall, Lord Beveridge, Canna,

and Pigou defined economics as a science of material welfare. In other words,

economics is a field of social science that studies how man uses accumulated wealth to advance material welfare.

Keynes defined economics as a field of

social science that studies the

management of limited production resource, determinants of national income, and

efficiency. In other words, it is the study of the causes of economic

instability and methods to achieve economic stability and growth.

Benham defined economics as a branch of

social science that examines the determinants of size, distribution and

stability of national income. Nowadays, studies on economic growth and

stability are becoming more important, especially for developing countries.

ECONOMIC RESOURCES

Economic resources are also known as

factors of production (input).

These resources are raw or man-made materials

used in the production process of goods and services (output).

Factors of production are limited in

nature.

Thus, society is only able to produce

goods of a limited quantity and is unable to satisfy all its wants.

Factor

of Production

(Resources,

Labour, Capital, and Entrepreneur)

Economic Resources 1: Land

Payments for resources: Rent

Description:

Land is a naturally occurring resource

(free gift of nature). It exists independent of human action.

The supply of land is inherently fixed in

location and geography.

The value of land is dependant on quality

and location.

Other examples are minerals, oil deposits,

timber, and water that exist on or below land/ the ground.

Economic Resources 2: Labour

Payments for resources: Wages

Description:

Labour is the physical and intellectual

services provided by man.

Labourers:

may be skilled or unskilled.

are unique and have feelings.

offer services, but are not to be

exploited.

can be moved from one location to another.

differ in efficiency and productivity.

Economic Resources 3: Capital

Payments for resources: Interest/Dividend

Description:

Capital consists of assets such as money,

equipment, machinery, and raw

materials.

Capital can be moved from one location to

another, and can be increased or decreased.

Economic Resources 4: Entrepreneur

Payments for resources: Profit (for the efforts and risks of entrepreneurship)

Description:

An entrepreneur is a person with the

skills and ability to organize production and bear risks.

An entrepreneur manages a firm and functions

as a leader, planner, and co-ordinator of the firm's activities.

CLASSIFICATION/TYPES OF GOODS

Goods are things which are tangible

or non-tangible. They are used to satisfy society’s wants or to produce other goods that

will satisfy the society’s wants. For example, goods that can satisfy human

needs are clothes, food, drinks, and cars. On the other hand, goods which are

used to produce other goods are machinery, buildings, and vehicles. Goods in

this list are tangible goods.

Non-tangible goods refer to air

and sunshine.

Services cannot be grouped as goods

because it does not exist physical. Nevertheless, services provide satisfaction

and fulfil society's wants. For example medical services provided by a doctor

to a patient, after-sales services (such as for computers), legal services and

hair dressing services do not exist physically but it fulfils the society’s

wants.

Goods can be divided into six categories: (i) economic goods, (ii) free goods, (iii)

public goods, (iv) finished goods, (v) capital goods and (vi) intermediate

goods.

Economic goods are scarce goods which the quantity demanded exceeds the quantity

supplied at a zero price and whose usage involves prices and opportunity costs. Economic goods

are divided into consumer goods and capital goods.

-Consumer goods or final goods are goods that yield satisfaction to the consumer. These items can be

classified into durable goods such as electrical fans and radios, or perishable

goods such as food.

-Capital goods are not intended for final use, but are used to produce other goods.

Examples of capital goods are machinery and factories.

Free goods or non-scarce goods are naturally occurring goods that are unlimited and

available without any cost. The quantity supplied exceeds the quantity demanded

at a zero price. Therefore, free goods do not have a price main and the

opportunity cost is zero. Free goods are essential for life, such as air and

water. However, due to pollution, clean air and water may no longer be free.

Public goods are non-excludable and are not subject to decisions made by individuals.

Individuals and communities are not exempt from using public of a c goods.

Examples of true public goods are powerhouses that are funded by the government

through taxation.

Finished goods are goods produced and used to satisfy society's wants. It can be

classified into durable goods (cars, televisions, refrigerators and furniture)

and perishable goods (vegetables, fruits and fresh produce).

Capital goods are goods used by consumers to produce other goods or for other specific

purposes. For example, printers are used to produce books and lorries are used

to transport goods.

Intermediate goods are goods which have not become finished goods and need to be further

processed before it can be used by consumers. For example, palm oil, timber,

cloth and steel. Intermediate goods cannot provide satisfaction to the

consumers.

FIELD OF ECONOMICS (MICROECONOMICS &

MACROECONOMICS)

The field of economics is divided

into microeconomics and macroeconomics.

Microeconomics

Microeconomics is the study of small

economic units, i.e. individuals and firms. The focus of microeconomic studies

or price theory is how economic agents such as individuals, households,

firms, and producers make economic decisions to achieve their respective goals.

Microeconomics also discusses how the prices of goods and factors of

production, wages, rents, and interest rates are determined.

Macroeconomics

Macroeconomics is the overall study of a

country’s economic activities and main economic sectors. Macroeconomics is also

known as the theory of income determination. A macroeconomic analysis focuses

on the economy as a whole. Macroeconomic studies focus on a general price

level, not on the prices of individual items. Problems are focused on consumption

and investment as the main variables in the theory of national

income. A measure of the national income of a country is the monetary unit.

Monetary studies involve studies on banks and national financial

institutions.

ECONOMIC PROBLEMS

There are three types of economic

problems: problems of scarcity, problems of choice, and problems of opportunity

cost.

Problems of Scarcity

Scarcity can be explained as wants which

are always exceeding limited resources meant to satisfy them. The needs or

wants are unlimited but the world has only a limited supply of natural

resources, time, energy, finances, and factors of production. Problems of

scarcity occur when goods and services are limited compared to

man’s unlimited wants and desires.

For example, Mat Lena has RM250,000

and he would like to open two new businesses: a restaurant and a bookstore.

However, he can only open one business because his capital is not enough to

support two businesses. In this case, the capital is a scarcity.

Individuals have problems of scarcity of

time for recreation, study, and entertainment, as well as scarcity of money

to pay for fees and to purchase food, drinks, and clothes.

Firms face problems of scarcity of capital

caused by limited economic resources. For example, a firm may not have

sufficient capital to carry out international projects.

The government faces problems of scarcity

of financial resources and revenue to build basic amenities for society such as

schools, clinics, and roads.

Problems of Choice

When there is scarcity, choices have to be

made. Everyone cannot have what he or she wants, so they have to choose from

the available alternatives. Individuals, firms, and governments make decisions

to choose from many alternatives. Since there are not enough available resources

to satisfy the wants of individuals and societies, individuals and societies

must make choices among competing alternatives.

For example, Mat Lena can make a

choice either to open a restaurant or a bookstore which would satisfy his

needs.

Problems of choice arise when we are faced

with problems of scarcity. Man has to make choices between desired goods and

services. Man also has to make choices between the usage of resources for the

present and the conservation of resources for the future.

Consumers need to make choices in order to

maximize satisfaction, while producers need to make choices in order to

maximize profits.

Unlimited demand is managed according to

priorities and rational choices based on an individual’s current budget.

For example, a certain amount of money can be used to purchase clothes or

shoes. In this situation, the individual spends the money on the item that will

yield the most satisfaction.

Firms make choices based on goals, i.e. to

maximize profits. For example, a firm can choose to open a new business or to

takeover an existing business.

Governments need to make choices based on

priorities to fulfil the wants of society. For example, a government can choose

to build either a hospital or a recreational park based on the amount of benefit

to society that each amenity can provide.

Problems of Opportunity Cost

Opportunity cost is the cost of one choice

in terms of the best forgone alternative. If you cannot obtain what you need,

then you have to choose among the alternatives. The next alternative that you

choose not to do is the cost of the thing that you choose to do. Opportunity

cost is also defined as the cost of not selecting the

“next-best” alternative.

For example, if Mat Lena chooses the

bookstore, then the restaurant is the opportunity cost because it is the second

best alternative which he has to forgo.

Problems of choice result in opportunity

cost. Opportunity cost arises from limited factors of production. For example,

an individual may have two options: to purchase a shirt or a pair of shoes. If

the individual chooses to purchase shoes, the opportunity cost is the shirt

that he/she is not able to purchase.

A firm may have two options, for example,

to open a new business or to takeover an existing business. If the firm chooses

to takeover an existing business, which will result in a higher profit, the

opportunity cost is the opening of a new business.

A government may have to choose between

constructing a hospital or a recreational park. The government may choose to

construct a hospital, which will provide more benefit to the public. In this situation,

the opportunity cost is the construction of a recreational park.

PRODUCTION POSSIBILITIES CURVE

Production possibilities curve is used to

explain problems of scarcity, choice, and opportunity

cost faced by a nation. This curve shows the maximum combination between two

different types of goods which can be produced by society based on the limited

factors of production and existing technological development (technology which

does not influence output). The shape of this curve is usually convex from its

point of origin.

Assumptions of Production Possibilities

Curve

The following assumptions are used to

explain the production possibilities curve:

There are only two types of goods.

Factors of production cannot be further

increased.

Level of technology is fixed or stagnant.

The economy has achieved maximum

efficiency (full employment).

Table 1.2 shows an example of the

assumptions for the production possibilities curve.

Table 1.2 Example of assumptions for

production possibilities curve

Assumption/Example

Fixed quantity and

quality of available resources

Mat Lena has a fixed supply of study materials such as textbooks, study

guides, notes, etc. to use in the available time.

Technology is fixed.

Mat Lena has a given level of study skills that allows him to translate the

review materials into exam scores.

There are no

unemployed nor underemployed resources

Efficient production is said to occur.

Table 1.3 Exam score for each class

Suppose that Mat Lena has four hours

left to study for exams in two classes: Economics and Calculus. The output in

this case is the exam score in each class as shown in Table 1.3.

|

| Table 1.3 Exam score for each class |

Each point on the production possibilities

curve in Figure 1.1 represents the best grades that can be achieved with the

existing resources and technology for each alternative allocation of study

time.

|

| Figure 1.1 Production possibilities curve representing Calculus grade and Economics grade |

The movement from point A to point B

results in a 30-point increase in Economics grade and only a 10-point reduction

in Calculus grade.

Since the opportunity cost of 30 points on

the Economics test is a 10-point reduction in the score on the Calculus test,

we can say that the marginal opportunity cost of one additional point on the

Economics test is approximately 1/3 of a point on the Calculus test.

|

| Figure 1.2 Production possibilities curve indicating movement from point A to point B |

The movement from point B to point C

illustrates the outcome if a second hour is transferred to the study of

Economics.

Transferring a second hour from the study

of Mathematics to the study of Economics results in a smaller increase in the

Economics grade (from 30 to 45 points) and a larger reduction in the Calculus

grade (from 75 to 55).

In this case, the marginal opportunity

cost of a point on the Economics exam has increased to approximately 4/3 of a

point on the Calculus exam.

|

| Figure 1.3 Production possibilities curve indicating movement from point B to point C |

Table 1.4 illustrates the law of

increasing cost.

The increase in the marginal opportunity

cost of points on the Economics exam as more time is devoted to studying Economics

is an example of the law of increasing cost. This law states that the

marginal opportunity cost of any activity rises as the level of the activity

increases.

Notice that the opportunity cost of

additional points on the Calculus exam rises as more time is devoted to

studying Calculus. Reading from the bottom of the table up to the top, you can

also see that the opportunity cost of additional points on the Economics exam

rises as more time is devoted to the study of Economics.

One of the reasons for the law of

increasing cost is the law of diminishing returns. Based on Table 1.4, each

extra hour devoted to the study of Economics results in a smaller increase in

the Economics grade and a larger reduction in the Calculus grade because of diminishing

returns to time spent on either activity.

|

| Table 1.4 Law of increasing cost |

The production possibilities curve will

change if there is a change in the following factors.

Additional Factors of Production

When there is an increase in the factors

of production, such as labour or capital, the economy will have a higher

capability to produce goods.

Figure 1.4 shows a production

possibilities curve with two types of goods, namely manufactured goods and

food.

The initial production possibilities curve

is curve AB. When there is an increase in the factors of production, the

production possibilities curve will shift outward to curve LK.

|

| Figure 1.4 Change in production possibilities curve as a result of increase in the factors of production. |

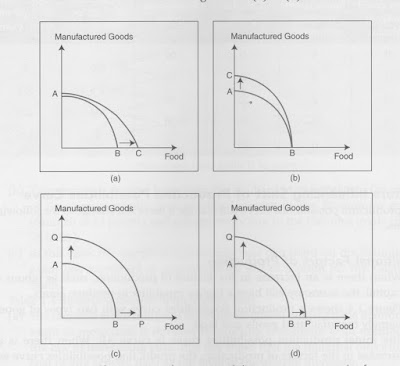

Progress in Technology

Progress in technology will shift the

production possibilities curve as shown in the four different scenarios in

Figures 1.5 (a) to (d).

The explanation for each graph in Figure

1.5 is as follows:

Progress in technology only occurs in the

production of food: shift from AB to AC.

Progress in technology only occurs in the

production of manufactured goods: shift from AB to CB.

Progress in technology occurs in the

production of manufactured goods and food: shift from AB to QP.

Progress in technology occurs in the

production of both goods but the rate of technology advancement is faster in

the production of manufactured goods than in the production of food.

|

| Figure 1.5 Change in production possibilities curves as a result of progress in technology |

Production Possibilities Schedule

Table 1.5 depicts the production

possibilities schedule for a country that produce two goods, food and clothing.

|

| Table 1.5 Production possibilities schedule |

The country has many options of

combinations in which goods can be produced simultaneously: A, B, C, D, or E.

For example, if combination B is selected, the country will simultaneously

produce 1 unit of food and 9 units of clothing (fully utilizing the country’s

factors of production).

When the production of food is increased,

the production of clothing must be decreased. For example, in the beginning to

produce 1 unit of food, the production of clothing must be decreased by 1

(10-9) unit. When the production of food is increased by 1 unit, the production

of clothing must be decreased by 2 (9-7) units. When the production of food is

further increased to 3 units, the production of clothing must be decreased by 3

(7-4) units. This situation occurs due to scarcity of factors of production in

the economy. Thus, the opportunity cost to produce additional units of food

will increase.

Interpretation of Production Possibilities

Curve

Production possibilities curve that is

downward sloping from left to right, as shown in Figure 1.6, illustrates a

negative or inverse relationship between the production of food and the

production of clothing.

The points A, B, C, D, and E indicate the

level of production that can be achieved with maximum efficiency of production.

Although point F is an achievable level of production, wastage and inefficiency

will occur. Point G indicates an unattainable level of production. At points A

and E, specialization will occur for the production of clothing and food

respectively.

The problem of scarcity is shown at the

right of the production possibilities curve, where the combination of goods and

services cannot be achieved (point G). The problem of choice occurs on the

production possibilities curve, i.e. the combinations of goods and services

that can be produced (points A, B, C, D, and E).

A downward slope from left to right on the

production possibilities curve indicates the problem of opportunity cost, i.e.

the amount of goods or services that must be forgone in order to increase

production of another good.

|

| Figure 1.6: Production possibilities curve |

Basic economic problems arise due to man’s

unlimited wants and limited factors of production. Man's unlimited wants have

resulted in four basic economic problems.

What Mix of Goods and Services Will Be

Produced?

In a market economy, the interaction of

self-interested buyers and sellers determines the mix of goods and services

that are produced.

There are insufficient available economic

resource to fulfil man's unlimited wants. Therefore, society must choose the

goods that will be produced and the goods that must be forgone at a certain

time.

The determination of the goods to be

produced by a country determines the pattern of allocation of available

economic resources to the various economic activities.

The pattern of allocation of economic

resources is determined to ensure that available economic resources are

efficiently used to produce goods and services to yield maximum satisfaction to

the economy as a whole. Apart from making choices about the types of goods to

be produced, society must also ensure that enough goods are produced to fulfil

unlimited wants.

The determination of the quantity of goods

to be produced is very important, as an increase in the production of one good

invariably results in the decrease in production of another good. Therefore,

society must ensure the sufficient production of every type of goods to fulfil

the wants of the economy as a whole.

Due to limited factors of production, not

all goods that a society demands can be produced. Therefore, the government’s

main aim is to ensure the production of essential goods for society.

How Much Goods and Services Should Be

Produced?

To overcome this basic economic problem, a

producer must identify the quantity of demand in the market.

If there is a high demand for a particular

good, the producer will increase production of the good. If there is a low

demand, the producer must decrease the production.

Therefore, a producer must make accurate

decisions about the quantity of the goods to be produced to avoid oversupply or

undersupply in the market.

Due to limited factors of production,

excess production results in wastage of factors of production. Therefore, the

government’s main aim is to ensure

sufficient production of goods and services.

How is Output Produced?

This question involves the determination

of the mix of resources that are to be used to produce output. In a market

economy, profit-maximizing producers will be expected to select a mix of

resources that result in the lowest possible level of cost (holding the

quantity and quality of output constant). New production techniques will be

adopted only if they reduce production costs.

Production techniques are divided into labour-intensive

and capital-intensive techniques. A producer selects a production technique

based on the relative costs of labour and capital.

If the cost of labour is less than the

cost of capital, the producer selects the labour-intensive production method.

If the cost of capital is less than the cost of labour, the producer opts for

capital-intensive production.

For Whom Should the Product Be Produced?

This basic economic problem deals with the

issue of “who gets what?”. In a market

economy, this is determined by the interaction of buyers and sellers in both

output and resource markets.

Generally, a producer produces a good for

people who can afford the cost of the good. This means that people with a

higher income will be able to afford more goods, while people with a lower

income can afford fewer goods.

Therefore, to ensure that society as a

whole can afford goods that are produced, the government should introduce a

fair distribution system.

SOLVING BASIC ECONOMIC PROBLEMS

In order to solve basic economic problems,

institutions or relevant bodies must

make decisions about how limited economic

resources are utilized to fulfil society's unlimited

demands. The solution to each basic economic problem is different for each

economic system.

What Mix of Goods and Services Will Be

Produced?

In countries that practise a free market

economy, the power of demand determines the goods to be produced. Goods in high

demand are produced in greater quantities.

In countries that practise a centrally

planned economy, the government determines the types of goods to be produced

based on the concept of welfare. Goods that provide welfare to society will be

produced in greater quantities.

Table 1.6 depicts solutions to the problem

of what goods should be produced for each economic system.

Table 1.6 Solutions to the problem of what

goods should be produced

Economic system/Solution

Economic system 1: Free Market Economy

Solution: Determined by the power of

demand or consumer spending patterns

Economic system 2: Centrally planned economy

Solution: Determined by the ruling

authority or government through a central planning institution. Individuals do

not have the freedom to determine the types and quantity of goods to be

produced

Economic system 3: Mixed economy

Solution: Determined by price mechanisms.

The government produces goods that are not produced by the private sector

Economic system 4: Islamic economy

Solution: Determined by price mechanism.

Individuals are free to choose or manufacture the types of goods to be

produced, subject to Islamic laws

How Much Goods and Services Should Be

Produced?

In countries that practise a free market

economy, the quantity of goods to be produced is determined by the price

mechanisms. The price mechanism system automatically determines the quantity

and price of goods to be produced, without government intervention.

In countries that practise a centrally

planned economy, the government through a central planning institution

determines the quantity of goods to be produced based on acquired economic data

and information.

Table 1.7 depicts solutions to be problem

of how much goods and services should be produced for each economic system.

Table 1.7 Solutions to the problem of how

much goods and services should be produced

Economic system/Solution

Economic system 1: Free Market Economy

Solution: Dependant on the price

determined by the market demand

Economic system 2: Centrally planned economy

Solution: Individuals do not have the

freedom to determine the types and quantity of goods to be produced. Priority

is given to the production of basic necessities and public goods

Economic system 3: Mixed economy

Solution: The private sector produces

goods based on price mechanisms. The government will supply public goods for

the use of all members of the society

Economic system 4: Islamic economy

Solution: Determined by price mechanism.

The government will supply goods that are not produced by the private sector

How is Output Produced?

Countries that practise a free market

economy generally use capital-intensive production techniques. The cost

difference between labour and capital is taken into account in solving this

basic economic problem.

Countries that practise a centrally

planned economy use labour-intensive production techniques to protect the

welfare of labourers.

Table 1.8 depicts solutions to be problem

of how goods should be produced for each economic system.

Table 1.8 Solutions to the problem of how

goods should be produced

Economic system/Solution

Economic system 1: Free Market Economy

Solution: Firms will choose a combination

of production factors to minimize costs. The determination of production factors is based on

the goal of maximizing output while minimizing costs.

Economic system 2: Centrally planned economy

Solution: Based on the government's goal of

achieving maximum output to fulfil the wants of society. The production

technique will also be chosen based on social welfare.

Economic system 3: Mixed economy

Solution: Firms will choose the production

method that will maximize profits and minimize costs. The government will

determine production methods based on current social benefits and social costs.

Economic system 4: Islamic economy

Solution: Firms will try to minimize

production costs by using the most efficient production techniques. However,

economic activities that are harmful to society are prohibited.

For Whom Should the Product Be Produced?

In countries that practise a free market

economy, goods are distributed based on ‘consumer's purchasing power! A wealthy

person has higher purchasing power compared to other people. This situation

creates a difference in status between the wealthy and the poor.

In countries that practise a centrally

planned economy, the government distributes income equally. This enables all

members of society to purchase goods fairly.

Table 1.9 depicts solutions to the problem

of for whom goods should be produced and distributed for each economic system.

Table 1.9 Solutions to the problem of for

whom goods should be produced and distributed

Economic system/Solution

Economic system 1: Free Market Economy

Solution: Determined based on individual's

purchasing power or income. Firms offer goods to parties that are willing to

pay the price.

Economic system 2: Centrally planned economy

Solution: Goods are distributed evenly and

fairly. The government controls prices or practises rationing policies to

ensure that each individual is able to enjoy goods that are produced.

Economic system 3: Mixed economy

Solution: Determined by price mechanism.

The income gap can be resolved through taxation and subsidy policies.

Economic system 4: Islamic economy

Solution: Goods are distributed based on

purchasing power and individual income. The government decreases the income gap

through alms, taxes, and subsidies.

MERITS AND DEMERITS OF ECONOMIC SYSTEMS

Free Market Economy (Capitalism)

Merits

Decisions are made quickly. All economic

decisions are made through the price mechanism. For example, market prices will

rise if there is increased demand, and market prices will fall if there is

decreased demand.

Incentive to work. Because all

profits are privately owned, producers work hard to accumulate wealth. In this

economic system, individuals are free to accumulate as much wealth as possible.

Economic efficiency. The concept of

efficiency refers to the maximum output that can be produced with

limited resources or input. Because the aim of a firm is to maximise profit,

the firm must ensure its production is always at a high level of

efficiency.

Competition. In this economic

system, firms are free to compete between themselves. This competition will

encourage technological innovation and advancement, which will contribute to a

higher level of satisfaction.

Demerits

Social welfare neglected. In

a free market economy, social welfare is often neglected, as firms are focussed

on maximizing profits. Social responsibility is often forgotten. For example,

firms will sell dangerous goods such as fireworks to consumers, as long as

consumers demand these goods.

Social goods insufficiently

produced. Social goods are non-exclusive. In other words, free market do not

produce all the goods that people want and are willing to pay for. There are

some goods and services whose benefits are social or collective, such as

national defence, open park areas, system of justice and police protections.

These are known as public or social goods. The fact that benefits of such goods

are collective presents the private market problems; once a social good is

produced, everyone gets to enjoy its benefits, whether they have paid for it or

not. Generally, the production of social goods increases the welfare level of

society, and do not generate profit. Therefore, the private sector will not

produce social goods.

Negative externality. Negative

externality is a negative external effect arising from uncontrolled industrial

expansion, for example, pollution of the environment. Pollution from disposal

of industrial wastes and toxic materials is a social cost to the local

community.

Wastage of resources. Wastage of

resources often occurs in a free market economy. For example, in a competition

between firms, advertising costs must be paid. If the advertisements are not

effective, the advertising costs are wasted.

Monopoly. Free competition between firms in a

free market economy may result in a monopoly. The emergence of a monopoly may

negatively impact consumers. For example, prices may rise, choices may be

limited, and goods may be of low quality as there is no competition.

Price instability. In a free

market economy, the government does not control prices of goods. Prices of

goods are determined by the power of supply and demand in the market. If demand

exceeds supply, the market price will increase. This price increase will burden

lower income consumers. The burden on consumers becomes more critical if the

good is a necessity. However, if supply exceeds demand, the market price will

fall. This situation will be detrimental to farmers who often face problems of

low prices for crops.

Wide income distribution gaps. In a free market economy), there is often a large income distribution

gap between the rich and poor. This may result in a disharmonious community,

which may affect the economic growth of a country.

Economists do not achieve full efficiency. Free market economists believe that unemployment will not occur in an

economy. If unemployment will occur, it will only be for a short period. In

theory, when an excess supply of labour occurs in an economy, wages will fall,

and when an excess demand for labour occurs, wages will rise. Finally,

when the supply and demand of labour are equal and equilibrium is achieved, and

the problem of unemployment will be solved. However, in reality, the supply of

labour always exceeds the demand for labour. Therefore, unemployment will always

occur in an economy.

Inefficient allocation of resources. In a free market economy, goods are not produced to fulfil wants, but

to reap profit. Not enough social goods that are important to increase the

welfare level of society are produced. In this situation, inefficient

allocation of resources will occur. The efficient allocation of resources will

happen when resources are used to produce goods that are genuinely needed by

society.

Conflict of opinions between the

private sector and the government. The conflict of opinions between individuals

(the private sector) and the government does exist when it comes to public

welfare. For example, education, health, infrastructure, police, fire brigade,

and army (defence) are the utmost concern of government, but on the other hand,

the private sector concerns more on producing goods and services for daily

consumption. The government produces the products that involve the security of

the nation like police service, the army, and the fire brigade.

Uneven distribution of income. The rich income group will continue to accumulate the wealth whereas

the condition of poor group will still remain as it was before.

Possibility of market and economic instability. Due to the quota system that has been introduced by government, the

tendency of misconduct in order to gain profit by the party concerned leads to

black marketing and price hike.

Emergence of illegal activities and negative external influences. Private sector in quest of making more than normal profit often involve

themselves in illegal activities and tends to avoid paying the penalties or

facing legal actions by the government, e.g. illegal selling, selling the

prohibited items, disposal of the toxic wastes, etc.

Possibility of inefficiency in use of

resources. Only few firms in private sector are interested in indulging social

activities as government intervention in business activities gives priority to

the welfare of community rather than the monetary gain.

Possibility of conflict between the

private sector and the government (strikes). The government will involve in

economic decision making to produce goods for public interest and national

security. Hence, there is a conflict of interest with private firms keen in

producing goods other than the interest of government and the public. This

creates dissatisfaction among the private firms that the creativity, innovative

and diligency is not paid off. The revenue is generally controlled by the

government, as a consequence the strikes may happen.

Centrally Planned Economy (Socialism)

Merits

Encourages mass production. The production

is up to maximum with minimum usage of factors of production.

Fair and even distribution of wealth and income. There will be no gap between the rich and the poor. This is because

individual has no freedom of owing the property and only the government

determines the distributions of the factor and income. Income distribution is

more equitable compared to other economic system. The main motivation of the

production is for the welfare of the society, not for the profit.

Production without competition. There will be a mass production determined by the government.

Creates the efficient use of resources and reduces wastage due to unhealthy competition. The resources are used efficiently for

the overall benefit of the society. Resources are not earmarked for the certain

segments of the society.

Creates economic stability. The welfare of

the society is the utmost technique of production. Therefore the unemployment

is minimal or does not exist.

Prioritises the production of public or social goods. The government provides more public goods because the economic

decisions are determined by the government.

Illegal activities and negative external influences reduced or

eliminated. This effect can be controlled by the

government, for example, traffic congestion, pollutions, etc.

Demerits

Errors in decision-making. The delay in

making the decision by government exists because the motivation of the

government is to give priority to the welfare of the people rather than the

profit of the company.

Lack of motivation and incentive to work. Productions are slow because of low motivation of the producers. Goods

are produced as per instruction of the government.

Development of technology and innovation not encouraged. Technological development and innovation are slow due to lack of

competition in the economy.

Limited individual choice. There is no

freedom in private ownership because all the properties and factors of

production are owned by the government. The producers only produce according as

per the wish of the government.

Bureaucratic planning and administration. The government plans and makes the decisions for all the economic

activities according to the wish of the people. The price is not important in

this system. The government decides the distribution by determining the prices.

Creates the possibility of inefficiency in the distribution of

resources. This economy does not create efficiency

in the productions. This is because the government gives priority to the human

resource rather than efficiency.

Lack of individual effort. The government

determines what and how much to produce according to the demand and welfare of

the people. There is no freedom to work because all the economic activities are

controlled by the government.

Lack of competition. Since the

production is controlled by the government, there is a lack of competition

among the producers to come out with the innovative ideas for the improvement

of goods and services in quality as well as variety. The wage and production

technique is predetermined by the government.

Mixed Economy

Merits

Co-operation between the public and private sector. In a mixed economy, the public and private sectors are involved in the

production of goods to satisfy the needs of consumers and increase social

welfare. The private sector produces goods for profit, while the government

produces goods for social welfare. Solving basic economic problems results in

efficient resource allocation and increased quality of life.

More options/choice. In a mixed economy,

the government produces public goods, while the private sector produces private

goods. Therefore, more types of goods will be produced in a mixed economy

compared to a free market society which only produces private goods.

Consequently, the quality of life in a mixed economy is relatively higher.

Efficient resource allocation. In a mixed economy, the government and private sectors compete with

each other to obtain resources and produce goods. However, the government can

intervene if competition for resources becomes unhealthy.

Social welfare prioritised. The government

will produce public goods and control the prices of public goods to ensure a

high quality of life. Because the private sector does not produce public goods,

the government will provide public goods to fulfil the needs of society. The

government will also ensure the welfare of lower income classes through

assistance, such as subsidies.

Prevention of control of monopolies. The government can overcome the power of monopolies through the price

mechanism and control the freedom of competition between firms. In a mixed

economy, the government can implement anti-monopoly laws and ceiling prices

(the maximum price that can be charged for a certain item), and implement taxes

on monopolies.

Guaranteed economic stability. In a mixed economy, problems of economic stability caused by the free

market economic system and price mechanism can be overcome. To ensure economic

stability, the government can implement fiscal and monetary policies. This will

ensure efficient use of resources and consequently ensure full efficiency.

Incentive to work. Individuals

and firms have the freedom to run economic activities and reap profits. Increased

efforts from individuals and firms increase a country's production and product

quality. Consequendy, the quality of life also improves.

Prohibition of illegal activities and negative external influences. The problems of illegal activities and negative external influences

that exist in a free market economy can be overcome through the enforcement of

laws and regulations by the government. Thus, the quality of life and social

harmony is ensured.

Production of public goods. In a free

market economy, public goods may not be produced. However, in a mixed economy,

the government produces public goods to increase social welfare levels. The

private sector does not produce public goods, which are capital-intensive,

involve high production costs, and require complex technology. Therefore, if

the private sector were to supply public goods, the high costs incurred would

affect the quality of life.

Demerits

Conflict of opinions between individuals (the private sector) and the

government. The conflict of opinions between

individuals (the private sector) and the government does exist when it comes to

public welfare. For example, education, health, infrastructure, police, fire

brigade and army/defence are the utmost concern of government but on the other

hand, the firms are concerned more on producing goods and services of daily

consumption. The government produces the products that involve the security of

the nation like police service, the army and the fire brigade. For the private

sector, it involves in the production of the consumer goods and services.

Uneven distribution of income. The rich income group will continue accumulating the wealth whereas

the condition of poor group will still remain poor as it was.

Possibility of market and economic instability. Due to the quota system that has been introduced by the government, the

tendency of misconduct in order to gain profit by the party concerned lead to

black market and price hike.

Emergence of illegal activities and negative external influences. Private sector needs more than normal profit will involve

themselves in illegal activities and to avoid from paying the penalties and

facing legal actions by the government, e.g. illegal selling, selling the

prohibited items, and disposal of the toxic wastes.

Possibility of inefficiency in the use of resources. Only few firms are interested in indulging in social activities since

government intervention in business activities gives priority to the welfare of

community compared to monetary gain.

Possibility of conflict between the private sector and the government

(strikes). The government will involve in economic

decision making to produce goods for public interest and national security.

Hence, private firms are keen in producing goods other than the interest of

both party. This will create dissatisfaction among the private firms that the

creativity, innovativeness and diligency are not paid off. The revenue is

dominated by the government and as a consequence the strike may happen.

Islamic Economy

Generally, Islamic economics is a branch

of social science that studies the unlimited desires of individuals to use

available resources to achieve happiness on earth and in the afterlife. It

studies how individuals and society use limited factors of production such as

land, labour, and capital to fulfil their unlimited desires. The Islamic

economic system is unique because of certain reasons.

Merits

Prioritises safety and happiness. The main aim of the Islamic economic system is to ensure safety and

happiness on earth and in the afterlife.

Eliminates economic activities having elements of interest (riba). The eradication of usury is the main responsibility of the government

as these practices are considered to be a form of oppression and cruelty,

particularly towards the poor.

Ensures social welfare. Wealth and possessions belong to Allah, and

man acts as a khalifah who is entrusted with responsibility to

safeguard the possessions. All economic activities that are not beneficial to

social welfare are forbidden. Welfare is the core of production.

Emphasizes happiness on earth and in the afterlife. Individuals are encouraged to seek profit through halal business

activities, i.e. activities that do not involve interest (riba) and are not

based on fraud.

Prohibits monopolies. Each member of

the community (in particular, the weak and the poor) is ensured the necessities

of life.

Distributes wealth and income fairly. Islamic principles emphasize the fair and equal distribution of wealth

and income. The right of each individual to basic necessities and to equal

opportunities is a unique characteristic of Islamic countries. The government's

main responsibility is to ensure that each citizen is guaranteed basic

necessities according to the principle of ‘right to life’ regardless of status,

race, or religion.

In a nutshell, characteristics of the

different economic systems are depicted in Table 1.10.

Table 1.10 Characteristics of different

economic systems

Characteristics/Economic systems

Characteristic 1: Ownership of resources

Economic system:

Free market - Privately

owned by individuals or the private sector

Centrally planned - Owned by

the government

Mixed economy - Freely

owned by individuals and the private sector, while partly owned by the

government

Islamic - Allah is the sole owner; man

acts as a trustee to utilize natural resources

Characteristic 2: Decision maker

Economic system:

Free market - Individual

Centrally planned - Government

and central planning institution

Mixed economy - Individuals

and the private sector (social goods), and the government (public goods)

Islamic - Individuals and producers,

based on Islamic principles and commandments

Characteristic 3: Price determination

Economic system:

Free market – Price mechanism

Centrally planned - Government

Mixed economy - Price

mechanism (private goods) and the government (controlled and public goods)

Islamic - Consumers and producers (power

of the market) based on Islamic principles and commandments

Characteristic 4: freedom to reap profits

Economic system:

Free market – Freedom to

reap profits resulting in high incentives to work

Centrally planned - No freedom

Mixed economy - Freedom to

produce private goods, but the government controls minimum profit rates for the

production of public goods (controlled and public goods)

Islamic - Freedom to seek profit, provided

that interest (riba) is not involved

Characteristic 5: Freedom of

choice

Economic system:

Free market – Individuals

and producers have freedom of choice

Centrally planned – Determined

by the government through central planning institutions

Mixed economy - Individuals

and private producers have freedom of choice (for private goods) and the

government makes decisions (for public goods)

Islamic - Individuals and producers have

freedom of choice, provided there is no contravention of Islamic principles and

commandments

6Characteristic

6: Production objective

Economic system:

Free market – To maximize

profits by prioritising individual interests.

Centrally planned – Priorities

social and community welfare.

Mixed economy - To

maximise profits (for private goods) and for social welfare (for public goods).)

Islamic - Prioritises the accumulation of

profit and social welfare based on Islamic principles and commandments.

SUMMARY

The study of economics can be defined as

the study of the behaviour of individuals and society in the utilization of

limited economic resources to produce goods and services to fulfil man's

unlimited wants.

Economic resources can be classified into

land, labour, capital, and entrepreneurship. The supply of economic resources

is limited, but there is an unlimited demand.

Man's wants are unlimited, but the supply

of economic resources is limited. Basic economic problems exist due to the

limited economic resources. Therefore, choices have to be made, resulting in

opportunity cost.

There are three basic economic problems:

what and how much should be produced, how a good should be produced, and for

whom a good should be produced.

The determination of what and how much

goods should be produced involves choosing between the productions of two

different goods.

The problem of how a good is to be

produced is related to the theory of production cost. A producer must decide

between labour-intensive or capital-intensive production techniques.

The problem of for whom goods should be

produced is related to how finished goods are marketed. Producers will sell

goods to consumers who can afford the said goods.

A production possibilities curve is a

curve that shows the maximum quantities of two goods that can be produced

simultaneously when all economic resources are efficiently utilized. The

production possibilities curve can be used to explain the concepts of

opportunity cost, changing levels of technology, efficiency, and choice.

A free market economy is an economic

system that does not involve government intervention in economic activities.

All economic decisions are determined by the price mechanism. Economic

resources are solely owned by private parties and are freely utilized by

individuals. Individuals and producers have freedom of choice.

A centrally planned economy is an economic

system that involves direct government intervention in the planning and control

of economic activities. Economic decisions are made by the government.

Consumers and producers do not have freedom of choice. Social welfare is

prioritised, resulting in the production of more social goods.

A mixed economy is an economic system

where the private sector and the government will make economic decisions

together. The government will intervene if there is any weakness in the price

mechanisms.

An Islamic economy prioritises a peaceful

Islamic community in every aspect of economic activities. Individuals are free

to accumulate wealth, in accordance with Islamic principles and commandments.

Related:

The Basic Economics Question - Given that we have relative scarcity it gives rise to

three basic economic questions faced by every economy. What to produce,

how to produce it and for whom it should be produced…

Fundamental questions in economics - Fundamental

economics are issues that are at the core of economics. They form the basis of

studying economics, such that if you are to study economics effectively at all,

then you have to understand these concepts fully from the very onset. Since

economics is studied from different perspectives, and since the many different

points of view often clash, the fundamental concepts also vary according to

particular school of thought. However, there are some concepts that are

conventionally accepted by most economists as very important. These concepts

come in the form of questions, which are referred to as the fundamental

questions of economics…

The Basic Economic Questions

- All economic systems that have ever existed or will

ever exist have to answer some basic questions...

What are the four basic economic questions? - The four basic economic questions

are: what goods to produce, how to use resources in the production process, who

receives the finished goods and when to produce the goods.

QUESTIONS

SECTION A: MULTIPLE CHOICE QUESTIONS

Answer all the questions below.

Choose one correct answer.

What

is the definition of Economics?

Economics

is defined as _____

A A study of social science that studies

man's behaviour in the distribution of limited factors of production.

B A study of the behaviour of individuals

in the determination of the optimum level of production at the minimum cost.

C The science of wealth in a community,

focussing on the distribution of factors of production and income.

D A study of social science that focuses

on behaviour of individuals in the allocation of limited production factors to

fulfil unlimited wants.

What

is the definition of Opportunity cost?

Opportunity

cost is defined as _____

A The cost of the second best option that

will have to be forgone in order to select the best option.

B The fixed cost involved in the short

term.

C The cost of using a factor of

production.

D The cost related to the optimum level of production.

Which

of the following services is not

available

in a free market economy?

A Educational services. B Transportation

services. C Defence services. D Medical

services.

In

a free market economy, production resources are allocated through____

A the power of supply and demand in the

market.

B the price mechanism and government intervention.

C production of profitable goods. D planning by firms and government intervention.

In

a centrally planned economy, the problem of for whom a good should be produced

is solved by___

A rationing. B market

mechanism. C market factors. D consumer

purchasing power.

In

a mixed economy, the problem of how much of a good should be produced is solved

by ____

A market mechanism.

B market mechanism and government intervention.

C production of public goods.

D the quantity of factors of production in the economy.

An

economy reaches productive efficiency when____

A production of a good can be increased

without reducing the production of another good.

B production of a good cannot be increased without reducing the production

of another good.

C economic resources cannot be fully

utilized.

D goods are produced in sufficient quantities to fulfil all consumer

needs.

The

figure below shows a production possibilities curve for the production of good

X and good Y. The points that indicate achievable production levels are points

Graph

(A) P and M. (B) F, G, (C) P, F,

and M. and K. (D)

F, M, and G.

Of

the following, which is not

a

merit of free market economy?

A Economic decisions are made quickly.

B Economic efficiency is achieved.

C Developments in technology and innovation are encouraged.

D Social welfare is prioritised.

Government

intervention is necessary in the economy because

A the government wishes to overcome

weaknesses in the free market economy.

B the government has power of monopoly.

C the government has interests in the

specific sector.

D the government wishes to share profits

with the private sector.

SECTION B: TRUE OR FALSE QUESTIONS

Answer all the questions below.

Macroeconomics focuses on aggregate

variables such as national income, employment and inflation. (True/False)

A product is said to be scarce if the

total amount needed by the society exceeds the total amount that the society

can obtain free of charge. (True/False)

When you make a decision to study

principles of economics, you incur opportunity cost. (True/False)

In the free market economy, all economic

decisions are determined by demand and supply. (True/False)

In centrally planned economy, production

resources are owned by individuals. (True/False)

The decreasing opportunity cost causes the

production possibility curve to have a concave shape. (True/False)

Capitalism is also known as free market or

laissez-faire. (True/False)

Scarcity occurs when our unlimited needs

exceed the ability to fulfil them due to limited resources. (True/False)

Finished goods are goods used by consumers

to produce other goods or for other specific purposes. (True/False)

Inferior goods are goods required by the

consumer for a comfortable lifestyle. (True/False)

Bilingual Glossary

macroeconomics

- makroekonomi

microeconomics – mikroekonomi

national income - pendapatan negara

rent - sewa

dividend - dividen

quantity

demanded - kuantiti diminta

final goods - barang akhir

quantity

supplied - kuantiti ditawar

interest - bunga

raw material - bahan mentah

price - harga

taxation - cukai

public goods - bahan awam

investment - pelaburan

variable - pemboleh ubah

bank - bank

economics - ekonomi

household - isi rumah

budget - belanjawan

goods - barang

benefit - faedah

labour - buruh

mixed economy - ekonomi campuran

production

factor - faktor pengeluaran

production - pengeluaran subsidy - subsidi

capitalism - kapitalisme

output - output

demand - permintaan

allocation of

resource - peruntukan sumber

excess demand - permintaan berlebihan

income

distribution - agihan pendapatan

profit - untung

socialism - sosialisme

capital - modal

normal profit - untung normal

DID YOU KNOW?

Nike  - Nike is the world's leading innovator in athletic footwear, apparel, equipment and accessories. Their mission is to bring inspiration and innovation to every athlete in the world. If you have a body, you are an athlete. This program offers a 7-day cookie duration.

- Nike is the world's leading innovator in athletic footwear, apparel, equipment and accessories. Their mission is to bring inspiration and innovation to every athlete in the world. If you have a body, you are an athlete. This program offers a 7-day cookie duration.

Old NavyUnder Armour - Under Armour is the leader in performance apparel, footwear, and accessories. Product are sold worldwide and worn by athletes at all levels, from youth to professional, on playing fields around the globe. The program offers a 30-day cookie duration.

UNIQLO

Michael Kors - Michael Kors is a world-renowned, award-winning designer of luxury accessories and ready-to-wear. The company currently produces a range of products under the signature Michael Kors Collection and MICHAEL Michael Kors labels. These products include accessories, footwear, watches, jewelry, men's and women's apparel, eyewear, and a full line of fragrance products. This program offers a 14-day cookie duration.

Ralph Lauren - RalphLauren.com offers great products for yourself and your home. You'll learn about adventure, style and culture in RL Magazine and on RL TV, find one-of-a-kind vintage pieces and exquisite gifts and more. This program offers a 14-day cookie duration. Take an extra 15% off for up to 50% off –ends May 3, 2016.

InterContinental Hotels Group - InterContinental Hotels Group is an international hotel company that provides popular hotel brands including InterContinental Hotels and Resorts, Crowne Plaza Hotels and Resorts, Hotel Indigo, Holiday Inn, Holiday Inn Express, Holiday Inn Club Vacations, Staybridge Suites, and Candlewood Suites with more than 4,200 hotels across nearly 100 countries. This program offers a 14-day cookie duration.

No comments:

Post a Comment